Millions of Americans have college debt but no degree: How to pay off your student loans

About a third of college students drop out, and they may be left tackling expensive student loan debt even without a degree to show for it. Here's how you can pay off your college debt with no diploma. (iStock)

Student loans are supposed to be an investment in your future earning potential, since a college diploma can grant you access to higher-paying jobs and better employment opportunities. But about 1 in 3 college students doesn't graduate within six years of enrolling, according to the most recent data from the National Center for Education Statistics (NCES).

As a result, the majority of college dropouts who took out federal or private student loans are saddled with debt, and no degree to show for it.

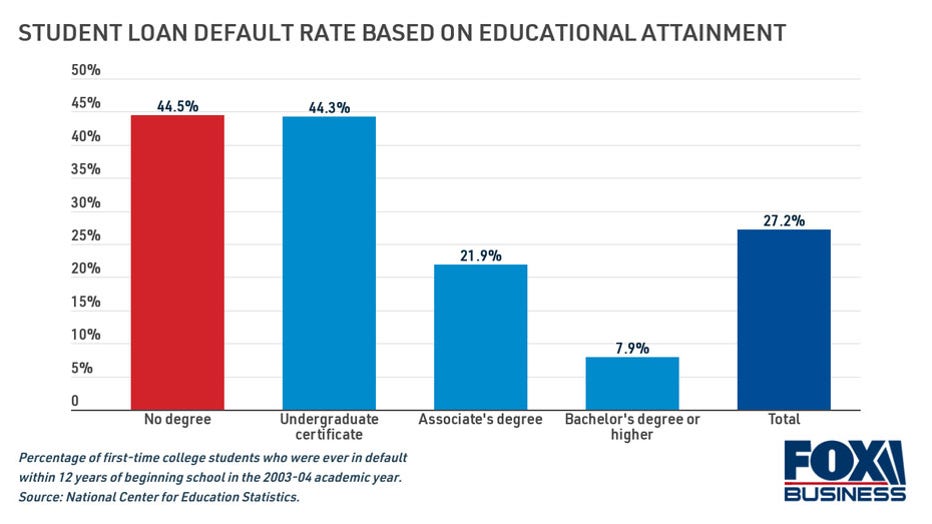

Student loan borrowers who didn't graduate are also much more likely to default on their loans than college graduates with a Bachelor's degree or higher, according to the NCES. Nearly half (45%) of student loan borrowers with no degree defaulted on their loans at some point within 12 years of beginning their secondary education, compared with 8% of graduates with at least a Bachelor's degree.

Getting rid of costly college debt may seem like an impossible task when you're limited by your earning potential. Even just staying out of default is a challenge for many student loan borrowers. But with student loan refinance rates at record lows, it may be possible to pay off your student loan debt once and for all.

Keep reading to learn how to get rid of college debt with no degree. If you decide to refinance, visit Credible to compare rates across multiple private lenders at once without impacting your credit score.

WILL BIDEN CANCEL STUDENT DEBT WITH AN EXECUTIVE ORDER?

What happens to student loans if you withdraw from college?

Put simply, there's no student loan refund policy when you drop out. Some universities have tuition refund policies that are prorated based on your withdrawal date, but for the millions of student loan borrowers who simply never graduated, college debt is a costly burden with no financial return.

Depending on the type of loans you have, you may be able to request assistance. Federal student loan borrowers can apply for economic hardship forbearance, unemployment deferment or loan rehabilitation. Even if you declare bankruptcy, though, you'll still owe your federal student loan debt.

Private student loans are sometimes discharged in bankruptcy, but they don't come with federal regulations and protections. College dropouts with private loans could consider refinancing to a lower interest rate in order to pay off their college debt faster or lower their monthly payments.

Use caution if refinancing federal loans, since doing so makes you ineligible for federal student aid programs like deferment and forbearance. But if you're struggling with unpaid private student loan debt, you have nothing to lose by refinancing, as long as you can secure a lower interest rate on your new repayment plan.

See examples of real student loan refinance rates in the table below. Then, check your eligibility and estimated rate on Credible to see if refinancing is right for you.

APPLYING FOR FAFSA IS ABOUT TO GET A LOT EASIER

Pay off your student loans faster by refinancing to a lower rate

Student loan payments can put a drag on your finances, especially if you're unable to increase your wages without a college diploma. Thankfully, it may be possible to pay off your student loans faster by refinancing.

Borrowers who refinanced to a shorter-term loan on Credible were able to shave 3.5 years off their loan repayment and even save nearly $17,000 in interest charges, due in part to lower interest rates. While this type of refinancing can save you money in the long run, it may slightly increase your monthly payment.

Remember that refinancing your federal loans makes you ineligible for federal aid, including forbearance and student loan forgiveness. But private loans don't have the same financial aid programs, so it's a safe bet if you can refinance to a lower interest rate.

Use Credible's student loan refinance calculator to determine your new repayment term, so you can decide if refinancing is right for you.

7 OF THE BEST LOANS FOR GRADUATE STUDENTS

Lower your monthly student loan payments by refinancing to a longer term

Defaulting on your student loans can be stressful and expensive. Interest charges and fees can add up over time when you're not making payments, and defaulting on your loans can have a lasting negative impact on your credit score. Plus, if your college debt is sent to a collection agency, you may risk being sued and having your wages or tax refund garnished.

One way to keep your student loan debt out of default is to lower your monthly payments by refinancing. Private student loan refinancing may be able to save you $250 or more on your monthly payment if you opt for a longer-term loan, which can help you stay out of default.

With student loan refinance rates hovering near historic lows, you may be able to save more money than ever before by securing a lower interest rate on your college debt. Get in touch with a student loan expert at Credible who can help you decide if refinancing is right for you.

HOW TO PREPARE FOR THE FREE APPLICATION FOR FEDERAL STUDENT AID

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.