Here’s how mortgage refinancing can save you an extra $5K with no adverse market fee

There's never been a better time to refinance to a new mortgage that has a lower interest rate than your original loan. Keep reading to see how the elimination of the Adverse Market Refinance Fee can help you take advantage of the low-rate environme

Homeowners can now refinance their mortgages without worrying about the added costs of a pandemic-era refinance fee.

The Adverse Market Refinance Fee was implemented by the Federal Housing Finance Agency (FHFA) in December 2020 to cover losses due to the COVID-19 pandemic. It added 0.5% to the cost of refinancing certain types of mortgage loans, which was passed on to borrowers in the form of higher interest rates.

But as a way to reduce housing costs, the FHFA announced on July 16 that it has ended the Adverse Market Refinance Fee earlier than expected, and mortgages originated today will not be subject to the fee.

Now is the perfect time to take advantage of historically low mortgage rates without being subject to the 0.5% fee. You can see your estimated refinance rates across multiple lenders by filling out a single form on Credible.

AVERAGE HOMEOWNER GAINS MORE THAN $30K IN HOME EQUITY OVER LAST YEAR

How much cheaper is refinancing now that the adverse market fee has been eliminated?

The Adverse Market Refinance Fee was charged to lenders on Freddie Mac and Fannie Mae mortgage loans. But the added cost would typically be passed on to borrowers.

If you were refinancing a $350,000 home loan, the 0.5% fee would add $1,750 to the total cost of servicing the loan. While some lenders may have just included this amount in the closing costs or added it to the total loan amount, others recuperated the cost by increasing your mortgage rate.

The fee amounted to approximately one-eighth of a point, resulting in a refinance rate that's 0.125% higher, according to the Mortgage Bankers Association.

On a $350,000, 20-year mortgage loan at 3%, for example, that small interest rate hike can add up. It would add about $20 to your monthly payment, increasing the total interest paid over the life of the loan by more than $5,000. But now that this fee has been eliminated on mortgage loans going forward, refinancing will resume without this added cost.

You can use Credible's online mortgage calculator to see how much the 0.125% rate difference would save you.

HOW TO BUY HOMEOWNERS INSURANCE

Mortgage lenders have already started lowering their rates

The adverse mortgage refinance fee won't officially be eliminated until August 1. But since mortgages that are originated today won't close until after that date, lenders have already started to adjust their rates for mortgage refinancing.

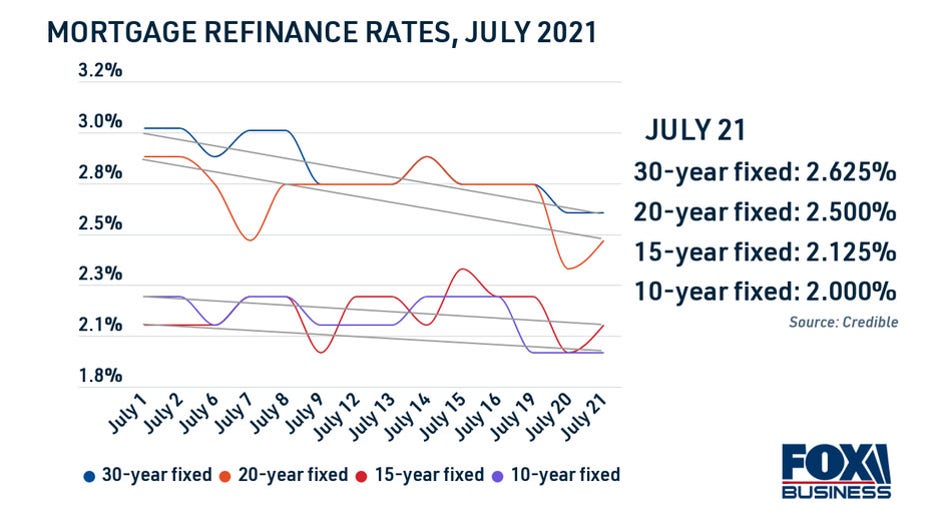

In fact, lenders have already started offering lower mortgage rates to well-qualified borrowers, according to data from Credible. Rates on a 20-year refinance hit an all-time low of 2.375% on July 20, and 30-year rates are holding steady near record lows at 2.625%.

The table below shows current mortgage rates from real mortgage lenders. See the refinancing rate you could qualify for without impacting your credit score by getting preapproved on Credible.

SHOULD I REFINANCE MY ADJUSTABLE-RATE MORTGAGE NOW?

Lock in your low mortgage refinance rate before rates inevitably increase

Mortgage interest rates are determined by a number of factors, including the borrower's credit score, the loan amount and the loan's term. But rates are also affected by circumstances that are out of your control.

Mortgage rates are heavily impacted by demand, as well as the Federal Reserve's interest rate on the 10-year Treasury Yield. The Fed has kept rates low to kickstart economic recovery during the coronavirus pandemic but it's expected to implement two rate hikes by 2023.

As a result, experts predict that mortgage rates will rise within the next few years. The MBA forecasts that 30-year mortgage rates will reach 4.2% in 2022 and 4.9% in 2023.

Act now to make sure you don't miss out on today's mortgage rates, which remain at historic lows. You can get in touch with a knowledgeable loan officer at Credible to begin the mortgage refinancing process so you can get a lower rate on a new loan.

WHAT IS PRIVATE MORTGAGE INSURANCE (PMI) AND HOW DOES IT WORK?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.